The global oil and gas pipes market is standing at the precipice of a transformative decade, driven by surging demands for specialized energy infrastructure, advanced drilling techniques, and comprehensive pipeline modernization efforts worldwide. Evaluated at an initial USD 63.0 billion in 2025, the global market is projected to expand significantly to reach USD 81.0 billion by 2035. Oil & Gas Advancement notes that this absolute growth of USD 18.0 billion reflects a compound annual growth rate (CAGR) of 2.5% over the ten-year assessment period, equating to a 1.3-times expansion of the market’s total value.

Shifts and Changes in the Market Forecast: A Two-Phased Expansion

The decade-long forecast for the market is uniquely defined by two distinct phases of expansion, each characterized by specific technological shifts and operational changes.

Phase 1: Modernization and Integration (2025–2030) Between 2025 and 2030, the market is projected to grow from USD 63.0 billion to USD 71.3 billion. This initial surge will generate an absolute value increase of USD 8.3 billion, representing precisely 46.1% of the overall forecasted growth for the entire decade. The defining shifts during this period will be heavily rooted in pipeline infrastructure modernization and the adoption of advanced drilling technologies. The market will see a shift toward product innovation, particularly in seamless pipe manufacturing, alongside the introduction of highly resilient corrosion-resistant coating systems. Furthermore, this phase is marked by expanding integration across upstream exploration endeavors and complex midstream transportation applications.

Phase 2: Specialization and Automation (2030–2035) In the second half of the decade, stretching from 2030 to 2035, the market is forecast to jump from USD 71.3 billion to USD 81.0 billion. This phase adds another USD 9.7 billion, constituting the remaining 53.9% of the decade’s expansion. The narrative of the market will fundamentally shift toward the widespread deployment of specialized pipeline applications, which include advanced high-pressure pipe systems designed for hyper-specific drilling environments. An elevated focus on energy security technologies, highly automated installation protocols, and stringent pipeline safety standards will act as the core catalysts during these years, demanding comprehensive and integrated pipe solutions.

Fundamental Growth Drivers and Market Constraints

The fundamental reason the oil and gas pipes market is experiencing such resilient growth is its ability to radically optimize operations. Advanced and specialized pipe technologies typically deliver a massive 40-60% improvement in operational efficiency when compared to conventional infrastructure alternatives. This allows energy operators to scale their drilling and transportation capacities without necessitating overwhelming in-house infrastructural overhauls.. Government initiatives that strongly promote energy security and the modernization of upstream exploration, midstream transport, and downstream refining pipelines further stimulate this demand.

However, the market forecast also accounts for notable constraints. The expansion is partially impeded by incredibly complex regulatory requirements, particularly in deep-water drilling scenarios. Technical challenges regarding system complexity and specialized integration during massive, large-scale projects limit accessibility for smaller enterprises. Moreover, the high validation costs associated with compliant pipeline capabilities create substantial barriers, especially in developing regions where technical infrastructure and regulatory frameworks remain somewhat ambiguous.

Segmental Shifts: Type, Material, and Application

A deep dive into the market segmentation reveals a clear hierarchy in product preferences and material durability required for modern energy extraction.

By Type: The Dominance of Welded Solutions In 2025, the welded segment is projected to dominate the landscape, capturing approximately 55.0% of the total market share. This leadership is secured by advancements in fusion welding processes and highly automated manufacturing systems. Welded pipes offer critical operational benefits, maintaining consistent pressure ratings and ensuring structural integrity across diverse installation environments. Conversely, the seamless segment will maintain a robust 45.0% market share. Seamless pipes remain highly sought after for complex upstream and midstream operations requiring specialized high-pressure tolerances and enhanced structural integrity during massive drilling applications.

By Material: Carbon Steel Maintains Unrivaled Leadership Due to the uncompromising structural demands of global pipelines, carbon steel accounts for a staggering 70.0% of the market share in 2025. The sheer durability and specialized strength capabilities of steel-based materials make them indispensable for complex energy operations across both emerging and developed markets. Following carbon steel, the stainless steel segment captures a 20.0% market share, heavily favored for its unparalleled corrosion resistance and chemical compatibility, particularly in extreme environment applications. The remaining 10.0% of the market is held by the composite segment, which is increasingly utilized for specialized operations requiring lightweight profiles and advanced material science integrations.

Regional Market Forecasts and Geopolitical Shifts

The global forecast highlights specific geographical hubs that will drive adoption and dictate international market trends through 2035.

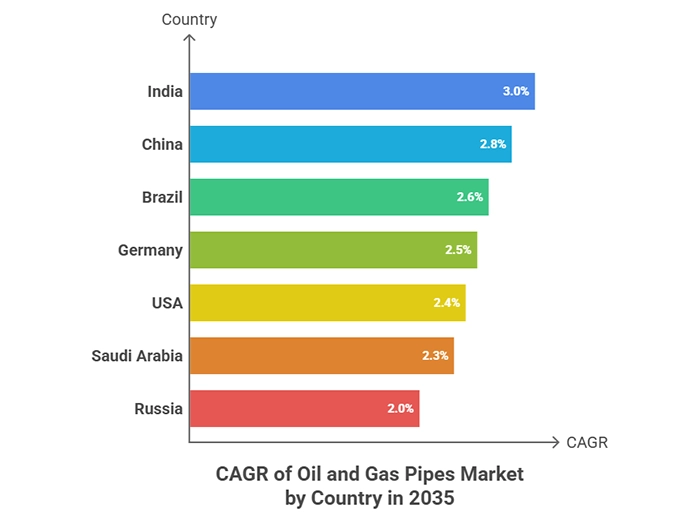

Asia Pacific: Leading the Global Charge India is positioned as the fastest-growing territory globally, projected to expand at a leading CAGR of 3.0% through 2035. This growth is heavily concentrated in massive industrial centers such as Mumbai, Delhi, Chennai, and Ahmedabad. The Indian government’s Ministry of Petroleum and Natural Gas provides critical policy backing for infrastructural modernization, enabling rapid adoption of advanced pipe systems. China follows closely with a highly robust 2.8% CAGR. Chinese operations are accelerating rapidly in centers like Beijing, Shanghai, Tianjin, and Guangzhou, where immense energy scaling, comprehensive modernization, and heavy government infrastructure programs mandate the use of next-generation pipeline solutions.

North and South America: Integration and Offshore Advancements In the United States, the market is set to grow at a steady CAGR of 2.4%. Growth in the USA is concentrated in rich energy regions like Texas, North Dakota, and Pennsylvania, where modernizing existing, aging pipeline infrastructure has yielded documented operational timeline improvements of up to 60%. Meanwhile, Brazil demonstrates strong energy innovation leadership with a CAGR of 2.5%. Brazil’s growth relies heavily on complex offshore drilling developments along its coastal areas, reporting a 25% annual increase in specialized pipe utilization for upstream and midstream segments.

Europe: Precision Manufacturing and Energy Security The collective European market is projected to expand from USD 15.2 billion in 2025 to USD 19.6 billion by 2035, growing at a 2.5% CAGR. Germany remains the undisputed leader in Europe, holding a 23.6% market share in 2025 and projected to grow at a 2.5% CAGR through 2035. Germany’s strength is anchored in its precision manufacturing hubs across Bavaria, Baden-Württemberg, North Rhine-Westphalia, and Lower Saxony, where intelligent pipe systems are aggressively adopted. The United Kingdom follows with a 16.7% regional share, France with 13.1%, Italy with 10.5%, and Spain with 8.3%.

Middle East & Emerging Markets: Saudi Arabia illustrates strong technology leadership, projected to grow at a CAGR of 2.3%. The nation is focused on precision and operational methodologies, yielding a 50% efficiency improvement across upstream facilities in regions like the Eastern Province and Riyadh. Furthermore, established markets like Russia (growing at a 2.0% CAGR) and mature sectors like Japan and South Korea continue to rely heavily on international tech partnerships and high-reliability seamless technology integrations to maintain global operational standards.

Future Outlook: Strategic Ecosystem Adaptations

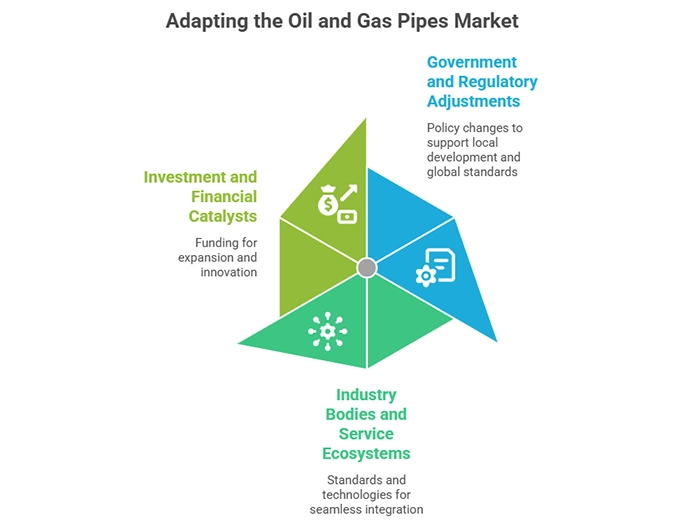

To fully realize the forecasted potential of USD 81.0 billion by 2035, the oil and gas pipes market ecosystem must adapt to incoming shifts. Without relying on specific corporate entities, the broader market will require coordinated evolution across multiple industry tiers.

Government and Regulatory Adjustments: Governments will inevitably need to adjust tax policies to spur local development, implementing accelerated depreciation schedules for specialized equipment and launching targeted innovation grants. Creating streamlined cross-border regulatory frameworks and heavily funding vocational skills training for pipe technicians will become mandatory to sustain the global pipeline network.

Industry Bodies and Service Ecosystems: Industry bodies will shift toward establishing universally recognized performance metrics and interoperability standards, ensuring seamless technological integration across varying regulatory environments. Service and technology providers must lean heavily into intelligence platforms incorporating predictive analytics, real-time performance tracking, and automated quality optimization to maximize pipeline lifecycles and meet stricter energy compliance demands.

Investment and Financial Catalysts: From a financial perspective, investors will unlock value by financing regional market developments, supporting strategic localized expansions to mitigate exorbitant installation costs. Venture capital is increasingly expected to back advanced seamless systems and highly intelligent pipeline startups, while broader strategic consolidations will create massive economies of scale capable of overcoming regulatory constraints in emerging territories.

In the opinion of Oil & Gas Advancement, the trajectory of the oil and gas pipes market from 2025 to 2035 points toward unprecedented technological refinement. By shifting away from mere infrastructural volume and focusing intensely on intelligent, specialized, and highly efficient systems, the industry is poised to fundamentally redefine global energy transportation and extraction over the next decade.

{kind=link}