The global energy landscape is currently undergoing a period of profound transformation, heavily influenced by shifting consumption patterns, evolving environmental mandates, and the continuous need for supply stability. In this highly dynamic environment, the physical infrastructure that supports global energy reserves is more critical than ever. The oil and gas storage market encompasses a wide array of specialized facilities meticulously designed to securely house crude oil, natural gas, and various refined products. In this comprehensive market report, Oil & Gas Advancement explores the fundamental economic drivers, technological innovations, changing material preferences, and shifting regional dynamics that are projected to define the industry from 2025 through 2035.

Market Valuation and Long-Term Forecast

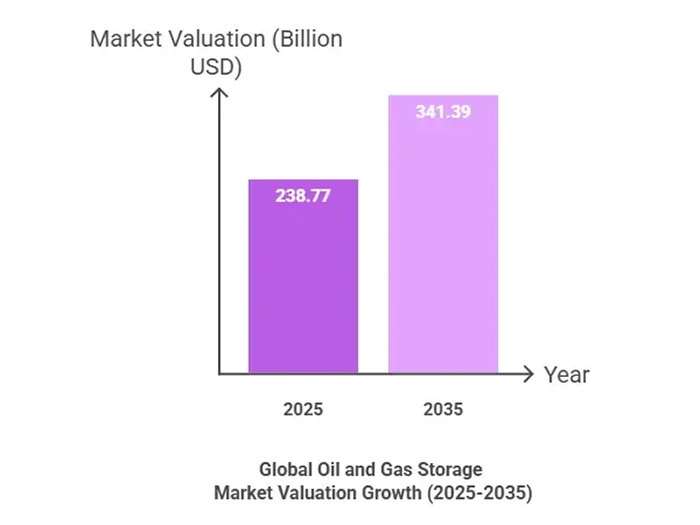

In terms of overall market valuation, the industry is poised for steady, reliable expansion over the coming decade. As of 2024, the market size was firmly established at an estimated USD 230.38 Billion. Stepping into the core forecast period, the market is projected to reach a valuation of USD 238.77 Billion in 2025 and is expected to continuously expand to a robust USD 341.39 Billion by the year 2035. This consistent upward trajectory represents a compound annual growth rate (CAGR) of 3.64% spanning the 2025 to 2035 timeframe. This growth curve underscores the persistent global reliance on traditional energy resources, even as the broader transition to alternative energy begins to take hold and reshape long-term strategic planning for infrastructure developers globally.

Primary Market Drivers: Energy Demand and Geopolitical Security

The continuous expansion of this market is heavily stimulated by multiple intertwined drivers, primarily the unyielding escalation in global energy demand. Driven by rapid population growth and widespread industrialization, particularly in developing economies, the fundamental need for reliable, accessible energy sources is intensifying at a rapid pace. Current macroeconomic projections suggest that total global energy consumption could rise by approximately 30% by the year 2040. To satisfy this immense appetite, drastically enhanced storage solutions are an absolute necessity. Furthermore, the inherent volatility of energy prices compels nations and facility operators to prioritize strategic storage to manage complex supply and demand imbalances effectively.

Alongside raw consumption demand, strategic geopolitical factors heavily influence future market dynamics. Tensions and instability in primary oil-producing regions consistently threaten to disrupt global supply chains, prompting nations to aggressively bolster their strategic reserves. A highly proactive approach to energy security has emerged across the globe; recent data indicates that various nations are actively enhancing their strategic petroleum reserves, with ambitious targets aiming to hold up to 90 days of net imports. This geopolitical imperative ensures a continuous flow of capital into the expansion and modernization of storage infrastructure to safeguard national economies against potential supply shocks.

Transformative Market Shifts, Trends, and Technological Integration

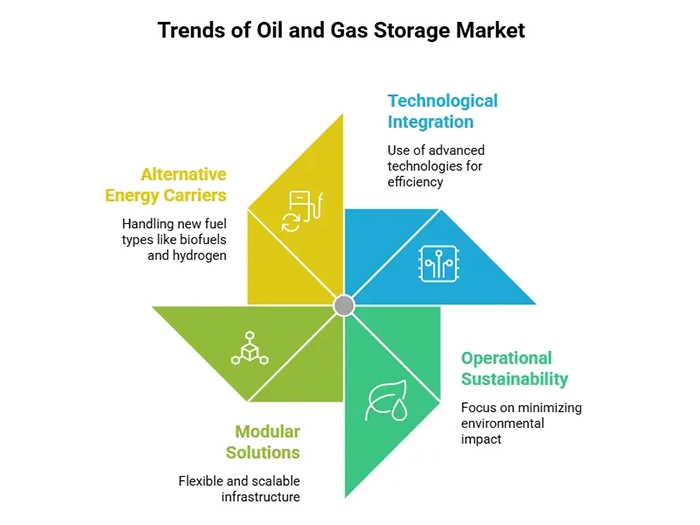

A major shift defining the future of the oil and gas storage market is the deep integration of technological innovation and facility digitalization. The industry is moving rapidly away from purely mechanical operations toward highly automated, intelligent frameworks. Technological advancements such as real-time monitoring, predictive analytics, and automated smart sensors are becoming standard operational requirements. These technologies allow for the exact, continuous monitoring of storage conditions, significantly reducing the environmental risks and operational costs associated with dangerous leaks and spills. Furthermore, there is a pronounced shift toward modular storage solutions, which afford operators critical flexibility and the ability to rapidly scale or deploy infrastructure as market demands fluctuate.

Simultaneously, the industry is navigating a monumental shift toward operational sustainability. Stringent regulatory frameworks and updated environmental standards are forcing a rigorous reevaluation of traditional storage methods. Governments globally are demanding minimized environmental impacts, often requiring costly structural upgrades like secondary containment systems. In response to the broader carbon-reduction movement, operators are integrating renewable energy sources directly into their storage strategies, paving the way for advanced hybrid storage models. The accelerated rise of alternative energy carriers, notably biofuels and hydrogen, requires highly innovative storage systems capable of safely handling diverse and complex fuel types, presenting both distinct engineering challenges and substantial growth opportunities over the forecast period.

Comprehensive Segmentation Analysis by Storage Type

Analyzing the market through the lens of storage methodologies reveals distinct preferences and emerging engineering tactics. Above Ground Tanks remain the dominant and largest segment in the market. Highly favored for their overall practicality, visual accessibility, ease of maintenance, and significantly faster installation times, these tanks cater effectively to diverse environmental conditions. This segment is expected to maintain the highest total valuation in the market. Below Ground Tanks represent another substantial, steady portion of the market. Floating Storage Units, which provide vital offshore flexibility for maritime transport, are expected to have some growth too.

However, the most strategically significant shift in storage methodology is the rapid emergence of Underground Caverns, which currently stand as the fastest-growing segment in the industry. As environmental regulations tighten globally and the sheer volume of required strategic storage increases, underground caverns provide unparalleled volumetric efficiency, space-saving benefits, and highly enhanced security with minimal surface-level environmental footprints.

Evolution of Material Types in Storage Construction

The choice of construction material is rapidly evolving as the industry attempts to balance traditional durability with modern efficiency and ecological needs. Steel remains the undisputed dominant material in the market, commanding the largest overall share due to its proven, multi-decade strength, longevity, and exceptional resistance to harsh environmental elements. The steel segment is fully projected to maintain its global leadership.

Conversely, Fiber Reinforced Plastic (FRP) is swiftly gaining massive traction as the fastest-growing material segment. As the market increasingly prioritizes logistical sustainability and operational efficiency, FRP offers highly appealing physical characteristics, primarily its significant weight reduction, superior resistance to aggressive chemical corrosion, and drastically lower long-term maintenance costs. The increasing capital investment in advanced material research is expected to further solidify FRP as a vital, innovative alternative for future infrastructure projects worldwide.

End Use Dynamics and the Rise of Cleaner Alternatives

The end-use segmentation highlights a global market currently in deep transition. Crude oil storage continues to represent the largest individual share of the market, rooted in deep-seated, consistent global demand and vast, pre-existing international infrastructure networks.

However, a pronounced structural shift is occurring as energy demands transition steadily toward cleaner alternatives. Natural gas has established itself as a dominant force, benefiting immensely from extensive new infrastructure projects and its critical role as a transitional bridging fuel. Within this specific spectrum, Liquefied Natural Gas (LNG) is explicitly identified as the fastest-growing end-use category, propelled by its increasing popularity as both a heavy industrial energy source and a high-efficiency maritime transportation fuel. Conversely, the refined products segment faces emerging structural challenges. While still fundamentally essential, its long-term growth is tempered by the accelerating global shifts toward vehicle electrification and zero-emission alternative fuels, forcing operators to pivot and innovate to retain market relevance.

In-Depth Regional Market Analysis

The geographical distribution of the oil and gas storage market is highly varied, with each macro-region presenting uniquely complex economic drivers, political constraints, and investment opportunities.

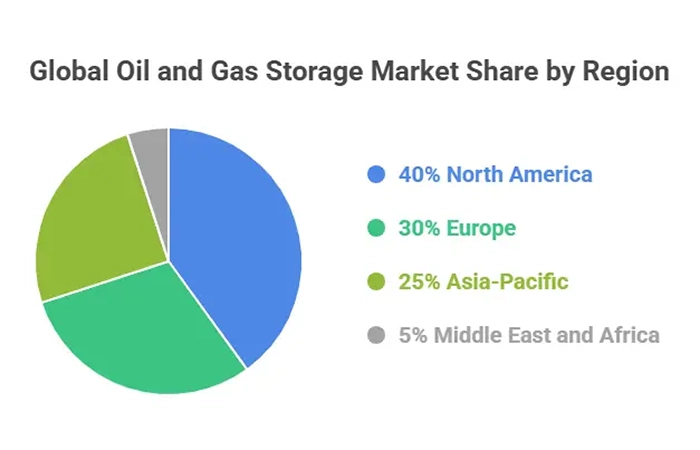

North America stands as the undeniable leader in the global market, controlling approximately 40% of the total market share. This massive economic footprint is supported by incredibly robust, well-established historical infrastructure, immense domestic energy demand, and highly favorable regulatory frameworks that aggressively support both traditional hydrocarbons and renewable energy storage developments. The region’s intense strategic focus on maintaining unparalleled national energy security ensures its continued infrastructure dominance throughout the forecast period.

Europe currently holds the second-largest global share, accounting for roughly 30% of the market. The European market is distinctively characterized by its rapid, aggressive transition toward sustainable, low-carbon energy. Guided by powerful, binding regulatory initiatives such as the European Union’s Green Deal, the region is pioneering the massive integration of renewable energy sources and innovative, low-emission storage technologies.

The Asia-Pacific region represents the most economically dynamic and fastest-growing territory, currently holding about 25% of the global market share. Driven by skyrocketing basic energy consumption, highly rapid urbanization, and massive industrial expansion particularly within highly populated emerging Asian economies the region requires vast new greenfield storage capacities. Governments across the Asia-Pacific are heavily focused on reducing their historical import dependency by building massive strategic petroleum reserves and establishing secure, highly localized storage infrastructures.

Finally, the Middle East and Africa, currently holding roughly 5% of the global market, provide significant, resource-rich growth opportunities. The region is witnessing a rapid influx of capital investment aimed at diversifying local energy economies and extensively expanding domestic storage capabilities. These expansions are designed to support broad macroeconomic national initiatives, ensuring long-term economic stability and energy security across the region.

Future Outlook and Strategic Conclusion

As the oil and gas storage market progresses relentlessly toward 2035, it is characterized by a delicate, highly strategic balance between fulfilling immediate, traditional global energy requirements and adapting successfully to a rapidly decarbonizing world. With a projected valuation of USD 341.39 USD Billion by 2035 and a solid, dependable CAGR of 3.64%, the sector is anything but structurally stagnant. The long-term future will be definitively shaped by the mass expansion of highly secure underground storage facilities in strategic locations, the widespread implementation of advanced, AI-driven leak detection and environmental monitoring systems, and the crucial deployment of modular, adaptable infrastructure for rapid scaling. By comprehensively embracing technological innovation, shifting toward dynamic hybrid storage models, and complying rigorously with stringent environmental standards, the global market is fundamentally set to remain incredibly robust. Oil & Gas Advancement believes this evolution will successfully facilitate the secure, reliable transition of global energy supplies for the next decade and far beyond.

{kind=link}